Quarterly investors letter – Q2 2023

Proving doubters wrong

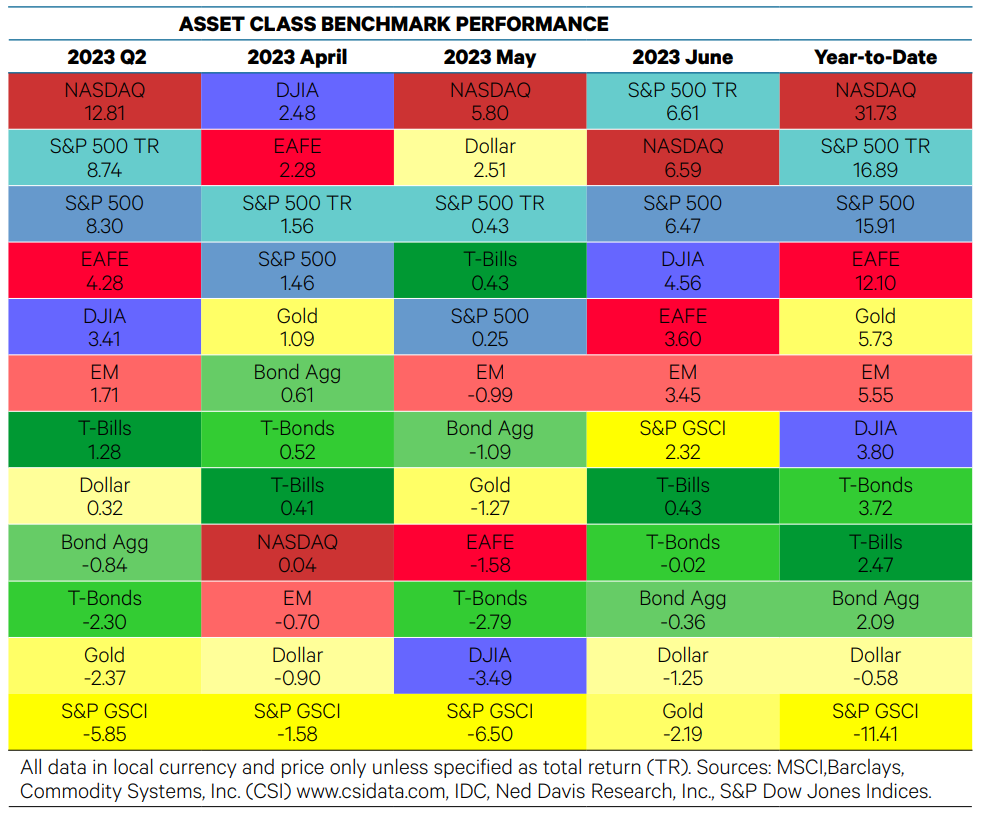

One of Wall Street’s adages – the market does what it needs to do to prove the majority wrong – came true in the first half. Coming into the year, the NDR Crowd Sentiment Poll was in the midst of its second-longest streak of extreme pessimism on record, after 2008-09. The Bloomberg survey of 25 Wall Street strategists showed a negative S&P 500 target for the first time since its inception in 1999. In spite of or perhaps because of this pessimism, the market staged one of its best first halves on record. The S&P 500 jumped 15.9%, the best since 2019, second best this century and 12th-best since 1926. The quick recovery from the regional banking crisis brought skeptics off the sidelines.

What does a strong first half mean for the second half? More often than not, positive momentum continues. When the S&P 500 rose at least 10% over the first six months, over the following six months, the index has risen 75% of the time by a median of 9.7%. Can there be too much of a good thing? History suggests yes. In the four cases the S&P 500 rose more than 20% in the first half, the index fell every time in the second half by a median of 6.5%; 2023 doesn’t fit this scenario.

Gold appreciated 5.7% in the first half but fell 2.4% in Q2 due to back-to-back declines in May and June. The move away from risk-off assets and prospects for more Fed rate hikes took the shine off the yellow metal. The supportive argument though, is that the latest FED monetary policy higher repricing has been welcomed by shallower corrections in the price of gold (see chart below). The S&P GSCI was the worst asset class on the table for Q2 and YTD, as supply chains adjusted and inflation slowed. The S&P GSCI is production-weighted, so it has a large weight in the energy sector. Meanwhile, the U.S. Dollar Index experienced some intra-quarter volatility but ended Q2 up 0.3% and is down 0.6% for the year.

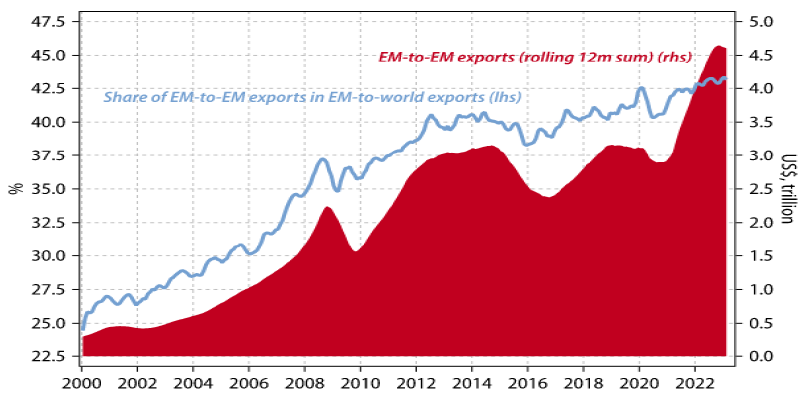

Despite the FED monetary headwind, the rationales underpinning our Enhanced Physical Gold strategy remain solidly valid. The Dedollarization trend continues to play out and the rising geopolitical tensions are adding momentum to it. We defined the current world order as bi-polar; the West & friends zone (US, Europe, JP…) and the Non-Western or The “Rest” countries. This second pole itself is made up of two zones. The opportunistic countries (Brazil, India, Saudi Arabia, Turkey, South Africa…) and the antagonist countries (Russia, China, Iran …). What the West sees as a deglobalization phenomenon is definitely not perceived as such from The Rest countries. Trade among The Rest partners has never been so buoyant, as have new infrastructure projects between them. A common feature of those enhanced linkages is the bypass of USD utilization as the traditional trade currency and the establishment of a different monetary order. Trade settlement, especially in the commodity space, takes place, increasingly, in local currencies, which in turn are finally recycled into local government bonds or gold, surely to a much lesser extent into US Treasuries.

Chart – Share EM to EM exports

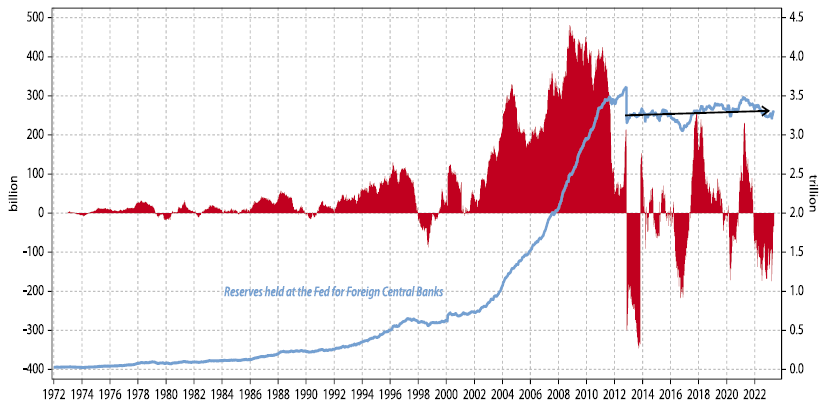

Probably the most important geopolitical event of 2023 is the restart of diplomatic relations between Iran and Saudi Arabia. The peace dividend in the Gulf area could also lead to a diminished allocation to USD reserves as the capital-intensive needs in military spending, directed to the US should abate (considering as well the transition from expensive military jets towards drones’ cheaper technology broadening utilization).

Chart – Reserves held at the FED by foreign CBs

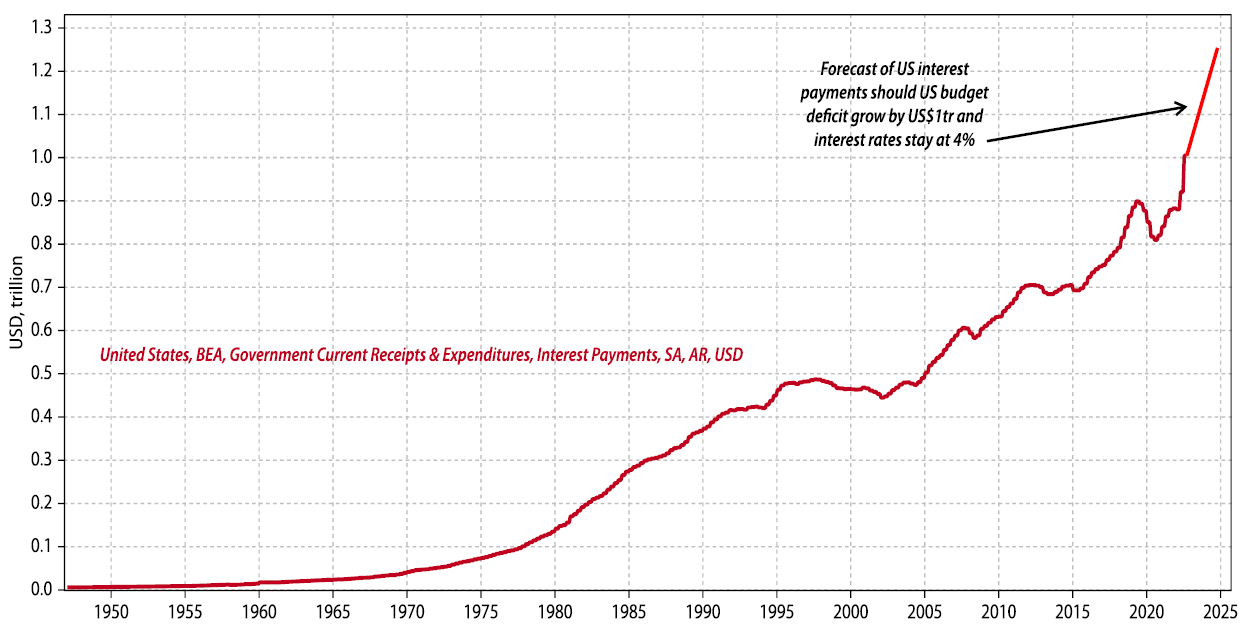

Inopportunely, the drying out of US Treasury buyers coincides with a US Treasury large issuance window. The US need to roll over half of its debt stock over the next two and a half years and given the trend in US rates, debt servicing is expected to grow by 10Bn USD per month over that same period. Given the shadow FED mandate of financial stability, (guaranteeing the government remains funded), debt monetization looks increasingly likely.

Chart – US Debt rollover

Chart – US Debt servicing costs

We would like to thank our long lasting research partners, GaveKal Research, Vincent Deluard, CFA StoneX and Ned Davis Research for their highly valuable contribution.

Sincerely yours,

Hans Ulriksen, CEO

Legal information

This document is intended for information and/or marketing purposes only. It is not intended for distribution to, or use by, any person or entity who is a citizen or resident of any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This document is not an offering memorandum and should not be considered a solicitation to purchase or invest in Noble Capital Management (NCM SA.

Disclaimer

NCM Enhanced Physical Gold Macro is a sub-fund of “NCM Alternative Assets, fonds à risque particulier” which is a contractual umbrella fund under Swiss law in the “other funds for alternative investments” category with specific risks. The sub-fund uses investment techniques whose risks cannot be compared with those of funds with traditional investments; in particular, the sub-funds may have significant leverage. Investors must be prepared to bear potential capital losses, which may be substantial or total. However, the fund management company and the asset manager endeavour to minimize these risks. In addition to market and currency risks, investors should be aware of risks relating to management, the negotiability of units, the liquidity of investments, the impact of redemptions, unit prices, service providers, lack of transparency and legal matters. These risks are detailed on pages 24 et 25 of the contractual fund.

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital.

For a comprehensive list of risks involved in investing in the NCM Enhanced Physical Gold Macro Fund, please refer to the Appendix of the Fund Contract. If you have any doubts about the suitability of an investment, please consult a financial adviser.

The information and opinions contained herein are provided for information and advertising purposes only. It does not constitute a financial service or an offer under the Swiss Federal Law on Financial Services (FinSA). In particular, this document is neither an advice on investment nor a recommendation or offer or invitation to make an offer with respect to the purchase or sale of the sub-fund and shall not be construed as such. Further, this document shall not be construed as legal, tax, regulatory, accounting or other advice.

The terms and conditions, the risk information and other details on the sub-fund are contained in the fund documentation, in particular the Fund Contract and its Appendix. The Fund Contract and the Appendix of the NCM Enhanced Physical Gold Macro Fund as well as the annual reports and any other product documentation may be obtained on request and free of charge from Noble Capital Management (NCM) SA or the fund management company.

This document has been prepared based on sources of information considered to be reliable and accurate. However, the information contained herein is subject to change without notice and this document may not contain all material information regarding the financial instruments concerned. No representation or warranty is made as to the fairness, accuracy, completeness or correctness of the information contained herein. Noble Capital Management (NCM) SA is under no obligation to update, revise or affirm this document following subsequent developments.

0 Comments