Quarterly investors letter – Q1 2026

Executive Summary – “Navigating a Regime of Shock and Dispersion”

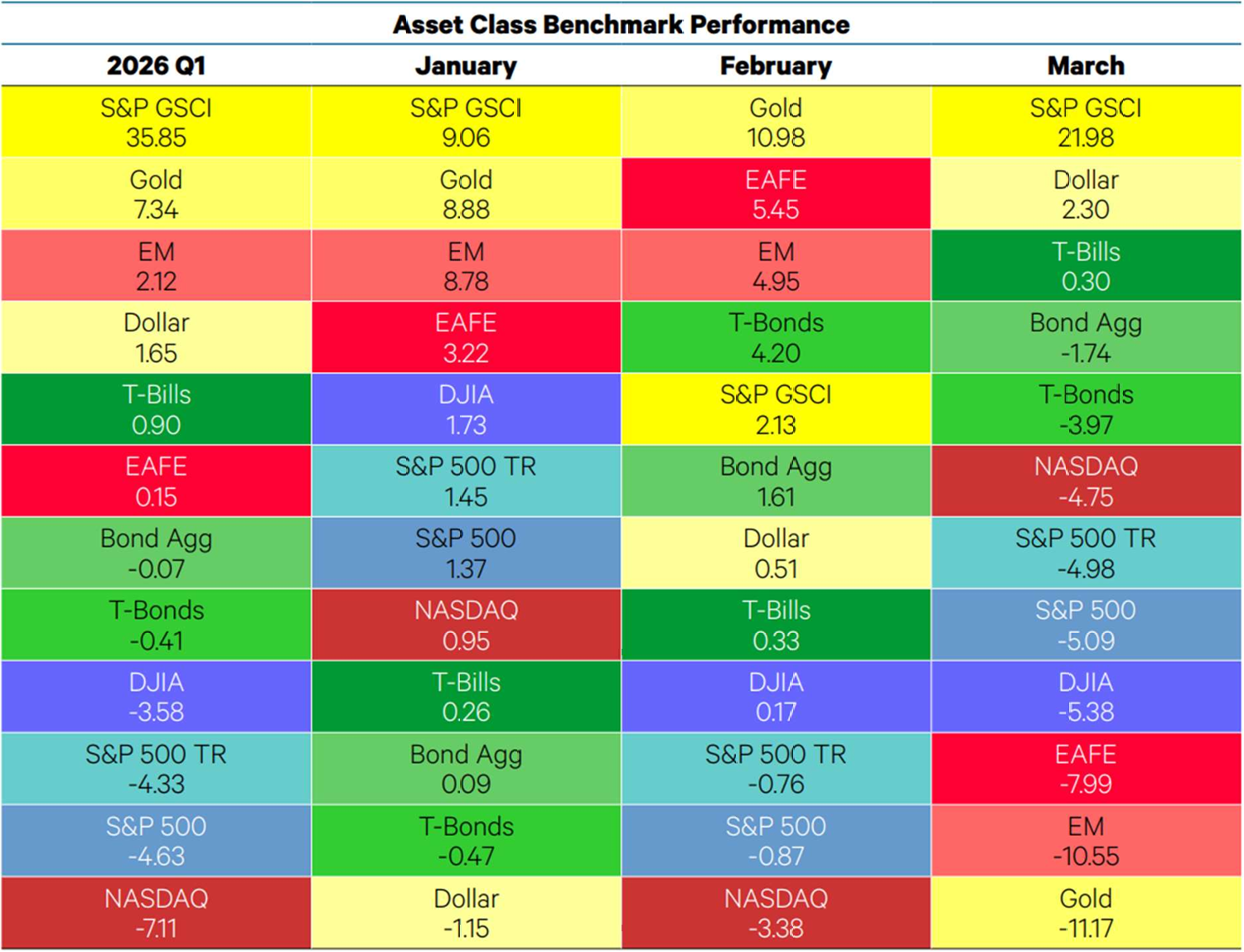

The first quarter of 2026 was defined by a sharp geopolitical repricing, a renewed inflation shock, and rising dispersion across asset classes and regions. The escalation of conflict in the Middle East triggered a powerful surge in energy prices, revived stagflation concerns, and exposed the fragility of traditional multi-asset allocations. Commodities were the clear outperformers, while equities and fixed income delivered mixed and often insufficient protection as markets adjusted to higher inflation expectations, tighter financial conditions, and a more complex policy backdrop. In this environment, performance was increasingly driven not by broad market direction, but by regional positioning, sector selection, liquidity management, and exposure to real assets.

Across our strategies, the quarter reinforced a core conviction: in a world shaped by structural inflation, geopolitical instability, and rapidly shifting narratives, resilience matters more than prediction. Our portfolios remained focused on diversification across regimes, disciplined risk management, and selective exposure to areas offering structural asymmetry, including commodities, energy, precious metals, and selected non-U.S. markets. While volatility rose sharply in March, we believe the quarter validated the importance of maintaining flexible, anti-fragile portfolios designed not for a single macro-outcome, but for a wider range of market conditions.

Global Market review

Commodities Surge Amid Strong Dispersion in Q1

In Q1, markets were shaped by a classic stagflationary mix of geopolitical risk, higher energy prices, and weakening performance from traditional multi-asset exposures. Commodities were the clear standout, with the S&P GSCI Futures Index rising 35.9%, driven by a sharp March rally following the escalation of conflict in the Middle East. Early in the quarter, gold and international equities also benefited from a defensive rotation, although both gave back relative strength in March as liquidity pressures and growth concerns intensified outside the U.S. The dollar, initially weak, reversed higher on safe-haven demand, while U.S. equities lagged both international stocks and core bonds. Even so, fixed income delivered only relative resilience rather than absolute protection, and Treasury bills once again outperformed both stocks and bonds. Taken together, the quarter reinforced the value of maintaining exposure to real assets and liquidity, while highlighting the continued fragility of the traditional 60/40 framework in an environment of persistent inflation pressure and geopolitical instability.

Key Asset Class Trends

The table below tracks returns for 12 asset classes across Q1, each month within the quarter, and year-to-date.

Equity Market & Fund Review

“War is the continuation of politics by other means.” — Carl von Clausewitz, 1832.

Equity markets in 2025: broad gains, uncomfortable truths

Q1 2026 was fought on 2 fronts. The first was geopolitical — the eruption of war in the Persian Gulf. with real bombs, real oil, real consequences. The second was informational— with presidential posts contradicting official briefings, ceasefire rumors reversed within hours, and markets repricing on statements before anyone could verify whether they reflected policy or impulse. Clausewitz wrote about the fog of war. We have something worse: a manufactured fog, produced at industrial scale, distributed algorithmically, and traded by machines faster than any human can establish a fact. But before the fog, the year began with unusual clarity.

January felt, for once, like a market making sense. The rotation that defined late 2025 — away from US mega-cap dominance — continued with conviction. Emerging markets gained nearly 9%. The ten largest S&P 500 stocks declined 0.9%. Equal-weight outperformed cap-weight. Value stirred after years of dormancy. For investors willing to look beyond Silicon Valley, the quarter began constructively. February introduced a different anxiety. The latest generation of AI models — cheaper, faster, and increasingly capable — began to look less like a tailwind for incumbents and more like a threat. US software stocks fell sharply. The top five S&P names declined 5.8% in a single month. Yet outside the US, momentum held: emerging markets added another 5%, Japan rose 8.6% in local terms, and Energy and Materials led globally. Dispersion quietly replaced direction as the market’s organizing principle. Then came 28 February — and the second front opened.

What made the shock particularly brutal was the context in which it occurred. The US-Israeli military campaign against Iran did not follow a conventional escalation path and instead began while diplomatic channels were still formally active. Envoys were meeting in Geneva. Markets were calm. Oil was contained. Then, abruptly, a full-scale military campaign was launched across Iran — political leaders assassinated, cities struck, infrastructure targeted — while diplomacy was still nominally ongoing. Iran responded with drone and missile attacks on US bases and Israeli territory. The Strait of Hormuz — through which roughly 20% of global oil supply transits — was effectively closed. Brent crude crossed $100 on March 9th and peaked near $126, marking the largest monthly increase in four decades. The IEA described it as the most severe energy security shock in history.

Markets reacted sharply and asymmetrically. In March, the US declined 4.9% and Europe 11.3%, erasing 2 months of gains in 30 days. For the quarter, the S&P 500 fell 4.3%, European equities 2.3%, and emerging markets were broadly flat at -0.1%. The Bloomberg Commodity Index surged 24.4%. Bonds offered no protection: yields rose as rate cut expectations collapsed. The stagflation trade — long dismissed — returned decisively. Throughout this period, the second front intensified. The presidential feed oscillated between escalation and negotiation, often within hours. Officials contradicted one another publicly. The Pentagon described one reality; the White House posted another. Markets were not only repricing military escalation; they were also repricing an unusually erratic policy-communication regime in which statements, reversals, and informal signaling became material drivers of volatility.

Fund Review – We do not predict. We adapt.

In an environment where narrative shifts faster than underlying reality, a rules-based framework that ignores narrative and focuses on price is not just useful — it becomes essential. When signal to-noise approaches zero, decoding the signal becomes futile. The discipline is to observe price, manage risk, and hold positions for structural reasons, not for what was posted overnight.

This antifragile philosophy guides the fund: position for probable risks, build resilience across scenarios, and avoid concentrated bets requiring a single outcome. It depends on being right about structure. Entering 2026, this framework translated into a neutral stance on US mega-cap and a relative overweight to emerging markets, European banks, Latin America, Nordic markets, and global refiners. Not because we anticipated war, but because valuations were more compelling and concentration in cap-weighted indices had reached historically unstable levels.

January and February validated this positioning. The NCM Global Equity Selection Fund gained 3.52% in January versus 2.79% for the benchmark, outperforming 92% of peers, with Latin America contributing 70 basis points. February added 1.79% versus 1.15%, as the correction in US mega-cap technology had limited impact on a portfolio already positioned elsewhere. By the end of February, the fund was up 5.37% year-to-date versus 3.97% for the benchmark. March presented a materially different environment. As the scale of the conflict became clear, we reduced portfolio beta and implemented a decorrelated FX hedging strategy. Our systematic overlay, designed to perform in periods of elevated volatility and behavioral dislocation, contributed positively. The fund declined 6.55% versus 7.12% for the benchmark. For the quarter, performance stood at -1.54% versus -3.43%, ahead of 80% of peers.

Since inception in October 2021, the fund has returned +28.88% versus +39.45% for the Bloomberg World Index — a gap explained by not participating in the massive US outperformance of 2022–2024. This was a deliberate choice, consistent with a framework that avoids chasing the final stages of a regime. Since early 2025, that relationship has begun to reverse.

Outlook and Fund Positioning – Two fronts, One Conclusion

On the 1st front — the Persian Gulf — markets continue to underprice the structural implications. The US entered the conflict with assumptions history has repeatedly challenged: that superior force delivers rapid resolution, that regimes collapse under assaults, and that exits are easy. Afghanistan, Iraq, Syria — none followed that script. Iran, larger and more cohesive, presents an even more complex challenge, with demonstrated asymmetric capabilities. The early signs are instructive: strikes on US bases, an aircraft carrier sidelined, F-15 downed, and munitions depletion. These could be the opening chapters of a longer conflict, yet markets remain closer to the preface than the conclusion.

The economic impact is highly asymmetric. For Europe and Asia, the shock is stagflationary: higher energy costs and weaker growth, leaving central banks constrained. The ECB, previously expected to ease further, now faces the possibility of tightening. For the US, the dynamic is structurally different. As a major energy exporter, higher oil prices transfer income domestically. A $1.2 trillion defense spending request adds further fiscal support, making the shock expansionary in the US while contractionary elsewhere.

Two structural shifts are accelerating. First, European energy independence — including nuclear — has moved from aspiration to necessity. Second, OECD defense spending is increasing at a pace reminiscent of the Cold War, with procurement shifting toward cost-efficient, AI-enhanced, asymmetric capabilities. For long-term investors, both represent durable trends to watch.

On the 2nd front — the feed — the conclusion is more reassuring. Despite unprecedented informational noise, markets continue to function. Volatility has increased but remains contained. Liquidity is intact. Price discovery is operating. The behavioral patterns — momentum, mean reversion, risk rotation — remain observable and exploitable. When official communication becomes unreliable, markets appear to develop a form of immunity. They do not eliminate volatility, but they process it. Our systematic models performed well during March. We maintain them.

Our positioning reflects both the geopolitical and informational fronts. We maintain a meaningful non-US overweight: energy producers, global refiners, defense-related industrials, and European banks — beneficiaries of higher inflation and yields. We now hold a small allocation to a US oil services ETF for direct operational leverage to energy upside. Latin America remains a core conviction. US exposure is maintained broadly at market weight. The systematic overlay remains capped at 30%.

Clausewitz might revise his framework today. War is still the continuation of politics by other means. But politics itself has become the continuation of communication by other means. In such an environment, the most valuable asset for an investor is not superior prediction. It is a framework robust enough not to require one.

fund Fixed-Income Markets & Fund Review

Market Review

Fixed income markets delivered a mixed but ultimately resilient performance over the quarter, with a late rally in U.S. Treasuries helping stabilize broader benchmarks. The 10-year Treasury yield retraced from 4.44% to 4.30% by quarter-end, allowing the U.S. Aggregate to recover most of its March weakness and finish only marginally lower. Performance dispersion across sectors was pronounced: floating-rate Treasuries led gains as markets repriced a shallower Fed easing path, while agency MBS and other securitized assets benefited from supportive policy measures and tighter spreads. TIPS also outperformed, supported by their lower duration profile and firmer near-term inflation expectations. By contrast, credit markets lagged as concerns around slower growth, geopolitical risks, AI-related disruption in selected industries, and private credit spillovers weighed on sentiment across leveraged loans, investment grade, and high yield. International fixed income was the weakest segment for U.S.-based investors, as broad U.S. dollar strength created a significant headwind across developed and emerging market debt.

Fund Review

The NCM Fixed Income Opportunities Fund delivered a mixed performance over the quarter. Following a strong start in January and February, the fund retraced a large part of its gains in March amid a more volatile market backdrop. The period was characterized by a sharp repricing of the Fed’s expected easing path, alongside a broader upward shift in the yield curve as markets began to reflect firmer energy price expectations. The fund returned -2.04% in March, bringing year-to-date performance to +0.53%. Despite this pullback, the fund continued to outperform its benchmark by a meaningful margin, ahead by 160 basis points versus benchmark performance of -1.07% year to date.

Performance over the quarter was supported in particular by the short position in U.S. 10-year Treasury futures established in late January, which was intended to reduce portfolio duration and proved timely as rates moved higher. This position contributed materially to relative outperformance. In addition, our high-conviction sector positioning heading into 2026, most notably our overweight exposure to energy, generated positive returns and helped offset the correction in local-currency bonds in Latin America and South Africa, which had performed exceptionally well through the end of February.

Looking Forward and Fund Positioning

We expect volatility to remain elevated until greater clarity emerges on the U.S. strategy surrounding the Iran conflict and the extent of related supply-chain disruptions can be assessed with greater confidence.

In our view, such periods of dislocation also create attractive opportunities, and our flexible, opportunistic approach is well positioned to navigate this environment. Against this backdrop, we intend to add selectively to our supranational bond exposure in commodity-producing countries, taking advantage of the price correction seen in March. We believe these issuers stand to benefit durably from the recent surge in commodities, both through improved rate dynamics and stronger currencies.

We have also increased our allocation to the energy theme and are evaluating the implementation of a credit volatility carry strategy, which we believe offers compelling entry levels and meaningful upside potential as markets normalize. Finally, we remain attentive to technical market levels and stand ready to re-establish a duration hedge should energy price pressures become more firmly embedded in curve premia.

Precious Markets & Fund Review

Fund Review

The first quarter of 2026 marked a sharp but, in our view, non-structural correction across precious metals. After entering the year on exceptionally strong footing, the complex was hit by a violent repricing as markets reacted to a combination of rising geopolitical stress, higher energy prices, tighter financial conditions, and a more hawkish Federal Reserve stance. Rather than invalidating the broader bull market, the quarter clarified the sequencing of it: the market first treated the Middle East shock as an oil-led tightening event, not yet as a full systemic hedge event.

Gold weakened while oil rose, which at first glance appeared counterintuitive. In practice, the move reflected a classic first-phase shock dynamic. As Brent surged on escalating risks around Iran and the Strait of Hormuz, inflation expectations moved higher, the U.S. dollar strengthened, Treasury yields rose, and financial conditions tightened. In that environment, gold traded less like an immediate geopolitical hedge and more like a highly liquid reserve asset exposed to real rates, liquidity conditions, and shifting expectations for the Fed.

This pressure was reinforced by the Fed’s March communication. The market interpreted the FOMC stance as a hawkish hold, with policymakers emphasizing uncertainty around the Middle East shock and signaling that an energy-driven inflation impulse would not automatically be looked through. That combination pushed investors to reprice the expected easing path, lifting yields and the dollar further, and adding pressure across the precious metals complex. Gold corrected sharply, while silver and PGMs declined even more aggressively, reflecting their higher beta and thinner liquidity profile.

At the same time, the correction increasingly took on the characteristics of a liquidity event rather than an orderly macro adjustment. Gold was sold because it was liquid. As stressed participants sought to raise dollars and reduce risk, the marginal seller appeared to be the liquidity-constrained holder rather than the long-term strategic allocator. Fast-money deleveraging, dealer hedging, options and futures expiry, and fragile positioning all amplified the move. The violence of the selloff, followed by a sharp rebound once immediate escalation risks temporarily eased, strongly suggested a market overwhelmed by flows rather than one entering a durable bearish regime.

Our framework remains two-stage. The first stage is the one experienced during the quarter: oil up, yields up, dollar up, and gold under pressure. The second stage is the one we believe matters more for medium-term returns. If the geopolitical shock proves persistent, the market will eventually shift from focusing on delayed Fed easing to pricing weaker growth, tighter balance-sheet conditions, and a greater risk of policy constraint. In that environment, nominal rates would likely lag inflation, real rates would move lower, and the backdrop would become increasingly constructive for gold. Put simply: short war is an oil shock; long war is a gold event.

In our view, the broader bull case remains intact. Central-banks accumulation, fiscal imbalances, de dollarisation, and the re-monetisation of gold as strategic collateral continue to provide a strong structural foundation. The first quarter did not break the thesis; it forced the market through its most uncomfortable phase first.

Fund Review

The NCM Enhanced Physical Gold Macro Fund experienced a difficult but actively managed quarter as the sharp correction across precious metals weighed on performance. The drawdown reflected not only the decline in gold, but also the more severe selloff in silver and PGMs, which underperformed materially during the liquidation phase. Against that backdrop, portfolio construction remained disciplined, combining downside protection, tactical monetisation of volatility, and selective re risking into weakness.

Gold: The Core Exposure

Gold remained the structural anchor of the portfolio throughout the quarter. While we stayed fundamentally constructive on the metal, we maintained a meaningful hedge overlay in recognition of increasingly stretched positioning and heightened macro sensitivity. As of end of March, the hedge covers 60% of our long gold exposure, equivalent to roughly 30% on a live basis after delta adjusting the long put option book. This overlay helped contain part of the mark-to-market volatility during the correction, although it did not fully insulate the portfolio from the scale of the dislocation.

Importantly, while the hedge reduced net exposure mechanically, our underlying directional stance became more constructive into the selloff. We used the correction to add to our core gold book, increasing gross long gold exposure to 112%. In other words, net exposure came down through the hedge, but underlying conviction increased as the market reset technically and positioning became cleaner.

Silver and PGMs: Residual Drag, Preserved Conviction

As in 2025, non-gold precious metals remained an important component of the portfolio’s alpha architecture. However, during the first quarter of 2026, they were a relative source of weakness. Silver and PGMs corrected more sharply than gold as the market entered a broad deleveraging phase, reflecting their higher beta, lower liquidity, and greater sensitivity to forced selling. Although we had already reduced these exposures materially from the elevated levels reached in late 2025 and early 2026, the remaining positions still weighed on performance during the quarter.

That said, our medium-term conviction has not changed materially. We continue to view silver and selected PGMs as structurally attractive satellites within the portfolio, supported by supply discipline, physical tightness, and, in silver’s case, a uniquely powerful combination of monetary and industrial demand. The quarter’s underperformance was primarily a function of market structure and liquidation dynamics rather than a deterioration in the long-term investment case.

Energy Hedging and Tactical Trades

In parallel with the core precious metals book, we continued to use opportunistic and partially decorrelated positions to manage portfolio convexity and improve overall return asymmetry. Our Brent hedge, implemented through a zero-cost collar structure, contributed positively during the quarter and helped cushion part of the correction in precious metals. This reflected the same macro logic outlined in our market commentary: the geopolitical shock initially expressed itself more clearly through oil than through gold.

We also used the spike in implied volatility to monetise rich option premium through short gold puts and short silver strangle. This was a tactical expression of the view that the market had entered an oversold and disorderly phase, and that volatility pricing had become temporarily disconnected from medium-term fundamentals. These trades were designed not as a substitute for conviction, but as a way to harvest dislocation while preserving flexibility in portfolio construction.

Conclusion

The first quarter of 2026 was marked by a violent correction across precious metals, driven by a combination of geopolitical stress, hawkish macro repricing, tighter liquidity, and forced deleveraging. In this context, the Fund faced a difficult environment, particularly given the sharper underperformance of silver and PGMs relative to gold. Nevertheless, the portfolio remained actively managed and strategically consistent: hedges reduced downside, tactical trades monetised volatility, and the correction was used to increase underlying gold exposure. The fund ends the quarter up 8.3% vs 5.5% for gold.

Our core conclusion remains straightforward. The thesis has not broken. What the quarter demonstrated is that in the early phase of a geopolitical and inflationary shock, gold can temporarily trade as a source of liquidity rather than as an immediate hedge. We believe that distinction is critical. In our assessment, the recent drawdown was technical and flow-driven, not structural.

Looking Forward – Precious Metals: From Liquidation to Re-Acceleration

Our constructive view on precious metals remains intact, although the first quarter made clear that the path higher is unlikely to be linear. In the short run, the complex remains vulnerable to tighter financial conditions, a stronger U.S. dollar, and episodes of forced deleveraging. Over the medium term, however, the same structural drivers identified in our previous letters remain firmly in place and may ultimately be reinforced by the geopolitical regime shift now underway.

Gold: From Funding Source Back to Monetary Hedge

Gold’s first-quarter correction should be interpreted as part of an unresolved structural revaluation rather than the start of a durable reversal. During the recent dislocation, the market temporarily treated gold as a liquid funding source in a rising-liquidity-premium environment. But if geopolitical disruption persists, growth weakens, and inflation remains sticky, the macro regime is likely to evolve in a way that becomes increasingly constructive for gold. In such an environment, nominal rates would struggle to keep pace with inflation, real rates would move lower, and gold should reassert itself as the preferred liquid monetary hedge.

Silver: High Conviction, Higher Volatility

Silver remains one of our highest-conviction opportunities, albeit one that is likely to remain volatile. The first quarter reinforced both sides of that thesis. On the one hand, silver underperformed sharply during the liquidation phase, reflecting its higher beta, lower liquidity, and greater sensitivity to forced selling. On the other hand, nothing in the correction altered the structural case for materially higher prices over the medium term.

If anything, the geopolitical shock may strengthen that case. The war in the Middle East and the sharp rise in energy prices create a direct incentive for energy-importing countries to accelerate their drive toward greater energy independence. In practical terms, this means faster electrification of energy systems and renewed investment in solar infrastructure, where silver remains a critical input. As energy security becomes a strategic priority rather than simply an environmental objective, solar deployment is likely to be supported not only by decarbonisation policies, but also by national resilience considerations.

This reinforces an already constructive backdrop built on persistent supply inelasticity, limited substitution, and structurally strong industrial demand. Silver therefore retains a unique asymmetry: it combines monetary optionality with growing strategic relevance in the global reconfiguration of energy systems. In our view, the metal remains highly exposed to short-term liquidity shocks, but increasingly well positioned for strong medium-term upside as capital rotates back toward both hard assets and electrification-linked commodities.

Platinum and Palladium: Selective Opportunity After Forced Selling

PGMs remain more complex and more tactical than gold. Their first-quarter correction reflected the broader liquidation across precious metals rather than a decisive change in fundamental direction. Platinum continues to benefit from structurally tight supply and improving end-use demand, while palladium retains asymmetric optionality linked to supply concentration and geopolitical risk. That said, both metals are likely to remain more volatile and more regime-dependent than gold itself.

Conclusion

We enter the second quarter with stronger conviction, even if the market remains fragile in the near term. The correction in Q1 reset positioning, exposed the market’s liquidity fault lines, and created opportunities to rebuild exposure on more attractive terms. Our view remains that precious metals are not leaving their bull market; they are moving through a volatile but ultimately constructive transition phase. In that environment, gold remains the core, silver the highest-conviction satellite, and disciplined hedging remains essential to capturing upside while preserving capital integrity.

Strategic Thinking – The Fed’s Quiet Demotion

From Master Institution to Supporting Actor

Paul Volcker once kept a protest sign on his desk. It had been carried by protesters outside the Federal Reserve building in 1980, at the peak of his war on inflation, and it read: “Volcker, get your foot off our neck.” He reportedly loved it. It meant he was doing his job — imposing pain on an economy that had spent a decade learning to live with inflation, regardless of the political cost, regardless of who was screaming. That sign was the emblem of an institution that genuinely led. That believed its independence was non-negotiable. That understood the difference between accommodating the fiscal reality and capitulating to it.

Kevin Warsh is unlikely to cherish such a sign. Not because he lacks conviction — he is a serious, intelligent man. But because the institution he is inheriting no longer has the foot, the neck, or the institutional appetite to apply pressure to either. The era that sign represented is over. What Warsh’s arrival makes official is the quiet, gradual, and now largely complete demotion of the Federal Reserve from master institution to supporting actor.

To be clear this is not a story about hawks and doves. It is not a debate about whether the next Fed chair will be more or less aggressive on inflation, more or less tolerant of weaker growth, it is about power. Those are the conventional coordinates of central bank analysis, and they will fill many column inches in the months ahead. They are also, by and large, beside the point. The more consequential shift is institutional — and it did not begin with Warsh. Kevin is not the architect of this transition. He is its custodian.

The power erosion has been underway for years as already mentioned in these columns. The Federal Reserve long ago stopped functioning as the disciplining force on fiscal excess that Volcker embodied. Faced with structural deficits, rising debt, and the relentless refinancing needs of a sovereign that borrows more than it can plausibly repay at high real rates, the Fed retreated. It did not retreat loudly. It retreated through accommodation — through a posture that prioritized financial stability over fiscal discipline, that found reasons not to tighten when tightening was inconvenient, that gradually redefined its mandate to include outcomes that once would have been considered none of its business. Warsh’s arrival matters because it gives that evolution a name, a face, and an institutional form. In our view, a Warsh-led Fed would be more likely to formalise the long-running erosion of central bank independence than to reverse it.

From Banker to Insurer

The practical consequences are significant. Under Warsh, the Fed is expected to do less — considerably less. Rate decisions will become more sporadic. Forward guidance, which became the central bank’s primary tool after the financial crisis, will lose much of its relevance. Balance-sheet activism will fade outside moments of genuine systemic stress. The Fed will stop attempting to fine tune the business cycle and re-emerge only when instability threatens the broader financial architecture. In other words, it will shift from active manager to residual stabilizer. From central banker to insurer.

Insurers, by design, do not prevent the build-up of risk. They price it. They stand ready to absorb the consequences when risks become catastrophic. And crucially, by standing ready to absorb consequences, they enable greater risk-taking in normal times. A more passive Fed is not necessarily a more restrictive Fed. It can become, paradoxically, the institutional foundation for broader financial expansion — as regulatory easing allows commercial banks to absorb more government debt, as excess reserves migrate from the Fed’s balance sheet back into the banking system, as leverage quietly rises across the private sector. The Fed may shrink. The system around it may expand, especially by supporting banking deregulation.

Short-end rates, under this framework, are likely to settle close to inflation — somewhere around 2.5% to 3.0% — implying near-zero real rates at the front end. The cost of financing US debt declines without requiring explicit monetisation. The mechanism is subtler than that: the Fed simply stops resisting the fiscal arithmetic. Policy changes become rare. The endless cadence of speeches, projections, and forward guidance — that peculiar modern practice of a central bank managing markets by talking about what it might do — quietly fades. For investors accustomed to parsing every syllable of every Fed statement, this will feel like a strange silence.

The Treasury Steps Forward

Nature, and macro policy, abhors a vacuum. As the Fed retreats, the US Treasury advances. In a world of structural deficits and persistent refinancing pressure, financial conditions can no longer be understood as the product of monetary policy alone. Treasury issuance strategy becomes a core macroeconomic instrument — adjusting maturity profiles, concentrating supply at specific points on the curve, using targeted buybacks to influence long-end yields. Yield curve control does not disappear. It becomes less visible. It migrates from the central bank’s balance sheet to the Treasury’s playbook. This is still coordination — but no longer between independent peers. It is a system in which fiscal priorities define the parameters and monetary policy adapts around them.

What Markets Must Price

The implications for the dollar and for Treasuries are substantial — and not comforting. For markets, the key issue is not whether Treasuries lose liquidity, but whether they gradually lose some of the institutional premium historically attached to a genuinely independent central bank. If that premium erodes, the long-term implications for term premia, the dollar, and real assets are significant. Once monetary policy becomes aligned, even implicitly, with sovereign financing needs, the dollar’s credibility becomes exposed to fiscal arithmetic. Investors begin to assess the currency not only through inflation and growth, but through the sustainability of the institutional mix. Treasuries are unlikely to lose their depth or liquidity. But they may gradually lose part of the unquestioned safe-haven premium that has rested, for decades, on the presumption of a fully independent central bank.

The deeper meaning of the Warsh era is not what it will do. It is what it will stop pretending to be. The Federal Reserve will still exist. It will still intervene in crisis. It will still set the outer boundaries of financial conditions. But it will no longer seek to lead the system it once defined. Its role is changing from master institution to supporting institution — from the room where the decisions are made to the room that ratifies them.

Volcker’s protest sign was proof that the Fed was in charge. Its absence from Warsh’s desk will be equally eloquent.

Hans Ulriksen, CEO and Fund Manager Christopher Boudin de l’Arche, Fund Manager

Legal information

This document is intended for information and/or marketing purposes only. It is not intended for distribution to, or use by, any person or entity who is a citizen or resident of any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This document is not an offering memorandum and should not be considered a solicitation to purchase or invest in Noble Capital Management (NCM SA).

Disclaimer

NCM Enhanced Physical Gold Macro is a sub-fund of “NCM Alternative Assets, fonds à risque particulier” which is a contractual umbrella fund under Swiss law in the “other funds for alternative investments” category with specific risks. The sub-fund uses investment techniques whose risks cannot be compared with those of funds with traditional investments; in particular, the sub-funds may have significant leverage. Investors must be prepared to bear potential capital losses, which may be substantial or total. However, the fund management company and the asset manager endeavour to minimize these risks. In addition to market and currency risks, investors should be aware of risks relating to management, the negotiability of units, the liquidity of investments, the impact of redemptions, unit prices, service providers, lack of transparency and legal matters. These risks are detailed on pages 24 et 25 of the contractual fund.

Past performance is not a guide to future performance. Do remember that the value of an investment and the income generated from them can fall as well as rise and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital.

For a comprehensive list of risks involved in investing in the NCM Enhanced Physical Gold Macro Fund, please refer to the Appendix of the Fund Contract. If you have any doubts about the suitability of an investment, please consult a financial adviser.

The information and opinions contained herein are provided for information and advertising purposes only. It does not constitute a financial service or an offer under the Swiss Federal Law on Financial Services (FinSA). In particular, this document is neither an advice on investment nor a recommendation or offer or invitation to make an offer with respect to the purchase or sale of the sub-fund and shall not be construed as such. Further, this document shall not be construed as legal, tax, regulatory, accounting or other advice.

The terms and conditions, the risk information and other details on the sub-fund are contained in the fund documentation, in particular the Fund Contract and its Appendix. The Fund Contract and the Appendix of the NCM Enhanced Physical Gold Macro Fund as well as the annual reports and any other product documentation may be obtained on request and free of charge from Noble Capital Management (NCM) SA or the fund management company.

This document has been prepared based on sources of information considered to be reliable and accurate. However, the information contained herein is subject to change without notice and this document may not contain all material information regarding the financial instruments concerned. No representation or warranty is made as to the fairness, accuracy, completeness or correctness of the information contained herein. Noble Capital Management (NCM) SA is under no obligation to update, revise or affirm this document following subsequent developments.

0 Comments